This is the fourth in a series of five articles in which Michael Settas elaborates on the critically important distinction between universal health coverage (a policy objective) and the proposed National Health Insurance (a financing mechanism). He provides a high-level background to the country’s two major health assets, the private and public sectors, as well as a history of health policy since 1994 that has culminated in the contentious and now imminent National Health Insurance proposal. You can read the first, second, and third articles here and here and here.

This fourth article of five provides a high-level overview of the private health sector, a substantial and well-established industry generally delivering high quality care across the spectrum of clinical categories. It has, however, suffered from substantial cost increases over the past two decades and has areas of inefficiency that could be rectified with improved policies and revised regulations.

Access to care is predominantly pre-funded through private monthly contributions to medical schemes, with membership mostly garnered through compulsory employer group schemes, although around a third of membership is maintained voluntarily.

Virtually all care funded through medical schemes is delivered by private providers, who are regulated through the Health Professions Council of SA as well as various other legislation.

Medical schemes and their associated providers, such as administrators and managed-care organisations, are regulated exclusively by the statutory Council for Medical Schemes (CMS), which is mandated through the Medical Schemes Act (MSA) of 1998. The MSA has entrenched a rights-based framework, founded on these social solidarity principles:

- Open enrolment, i.e. no applicant can be denied cover regardless of health status or age;

- Lifetime coverage;

- Community rating, i.e. everyone pays the same contribution regardless of claims, health or age; and

- A minimum standardised package of cover (called the prescribed minimum benefits).

According to the latest annual report from the CMS, on 31 December 2020 there were 8.9 million people covered on 76 medical schemes, of which 18 are open schemes and 58 closed employer/industry-based schemes.

Medical schemes are private juristic entities governed by a board of trustees, and their assets are collectively owned by their members. They are also reasonably efficient funding vehicles as they are non-profit entities and exempt from paying income tax.

Typically, medical schemes do not employ the personnel or deploy the management and IT systems required to manage their operations, but rather outsource these to specialist third party administrators and managed care organisations (although there are a few exceptions to this practice). The typical cost of these ‘non-health’ functions ranges from about 8% to 12% of contributions, with the majority of the balance of contributions going towards paying medical claims (85-90% is typical).

Breakeven

Medical schemes usually budget to run at an operational breakeven, with investment income on their reserves creating small overall profit margins that bolster their solvency levels. The statutory minimum solvency level is 25% of annual contributions. According to the latest CMS annual report, schemes collectively received R219bn in contributions during 2020 and held just over R100bn in reserves on 31 December 2020. Reserves were bolstered substantially because of a large reduction in elective surgeries during the Covid-19 lockdown in 2020, but schemes have since delayed or reduced annual contribution increases, thus using up some of these excess reserves.

Accurately determining the number of medical personnel working in the private sector is complicated by various factors, but two calculations undertaken by consultancy Percept in 2019, on behalf of Business Unity SA, estimated the number to be somewhere between 69 000 and 116 000. According to a study by Econex (now FTI Consulting) in 2017, there were an estimated 40 702 private hospital beds in SA, providing a high ratio of 46 hospital beds per 10,000 insured members.

Access to care in the private sector is high, with waiting periods on elective surgery generally being unheard of.

The economics of healthcare

It is important to note that healthcare markets, particularly unfettered private markets, do not operate under the same economic principles as most other markets.

In regular markets, demand will lead supply, and any distortion of either will likely be met with a balancing reaction. These reactions will usually occur because of competition amongst suppliers and/or informed consumers, and in the absence of these factors, governments usually intervene to control prices and/or increase transparency.

In healthcare markets, the opposite occurs. Supply leads demand, a factor known as supplier-induced-demand, and there is significant asymmetry in knowledge between the providers and consumers of health services. Price controls seldom work in healthcare markets, as any restriction thereon can be countered by an increase in the volume of supply, known as over-servicing, especially because of the inherent knowledge asymmetry and fee-for-service remuneration models.

This requires that a health market be sufficiently well regulated on both the demand side (i.e. funders of healthcare services) as well as supply side (i.e. providers of healthcare services). The private sector currently lacks any meaningful form of regulation on the supply side, although this was addressed by the Health Market Inquiry (more on this later).

There is also a moral hazard induced by consumers of healthcare when they are insured (or have sufficient income to cover medical costs out-of-pocket). Certain patients will expect or even demand health services or medicines beyond their actual need, based on either a high-level of consumerism or innate levels of hypochondria. A perfect example of this is the excessive antibiotics that are unnecessarily prescribed in South Africa to patients with seasonal cold or flu symptoms.

Besides the obvious cost implications of this behaviour, it also dangerously heightens the risk of antibiotic- resistant infections, which can have life-threatening implications. These are often complex behavioural problems for both funders and providers to manage, but nonetheless they can cause significant problems in health markets.

Private Sector Cost Increases

By any measure, costs in the South African private sector have grown substantially in the past two decades.

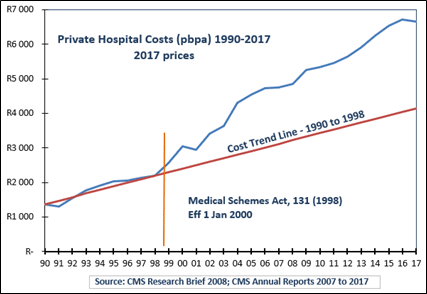

Since 2000, when the current MSA came into effect, the one common benefit category that all schemes have carried, quite comprehensively, has been hospital-based care. This allows for a fairly uniform analysis to evaluate these cost increases over time.

Graph 1 below shows private hospital costs paid by all medical schemes on a per beneficiary per annum basis from 1990 to 2017. These are reflected in real terms (2017 prices – blue line) with the red trend line showing costs from the 1990s projected forward to 2017. It is clear from this that there was a very substantial upturn in hospital costs as from about 1998/99, when the MSA was promulgated.

There was also a concomitant consolidation of private hospital beds in SA within the three largest hospital groups (Life, Mediclinic, and Netcare), increasing their collective share of ownership from about 55% of beds in 1998 to over 80% by 2004. This technically formed a highly concentrated market – an oligopoly which remains in place.

The social solidarity framework of the MSA provided considerable rights to consumers but was, and still is, crucially missing an essential pillar of a sustainable framework, i.e. mandatory membership. Had this provision been implemented in 2000, it would have meant that all formally employed citizens, or at least a substantial sub-set of the higher-earning formally employed, would have been compelled to belong to a medical scheme. This would have removed the ability for consumers to anti-select the system.

Graph 1

Maintaining the social solidarity framework of the MSA without mandatory membership meant that consumers could anti-select the system based on their current health status, i.e. older and sicker members typically would maintain cover, whereas younger and healthier members would opt out. Only once members outside the system had health needs above the cost of membership, would they seek membership which is guaranteed through the open enrolment provision of the MSA.

There is a counter-measure to this anti-selection – medical schemes can apply what is called a permanent ‘late-joiner penalty’ to the monthly contributions of a new member over the age of 35 with no previous cover. However, it is generally acknowledged that this penalty is unknown to the vast majority of uninsured citizens, so it is unlikely that the existence of this penalty provision has any influence on the level of medical scheme participation.

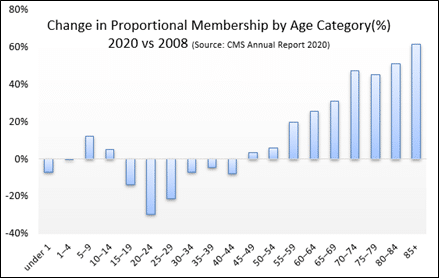

Graph 2

Graph 2 shows the predictable result – comparing membership by age category between 2020 and 2008, it is obvious that proportional membership from age 15 to 44 has fallen, whereas from 45 and older it has grown. In 2008, around 20% of all medical scheme beneficiaries were 50 or older, whereas by 2020 that proportion had grown to almost 25%. These changes have a dramatic impact on costs, since age is the most significant driver of health costs.

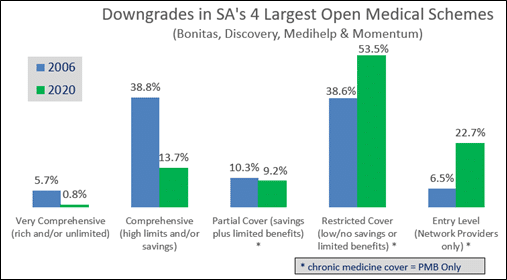

In response to these cost pressures, medical schemes have reduced benefits and narrowed the range of clinical benefit categories covered, in order to keep monthly contribution increases as low as possible. The number of benefit options offered by medical schemes has also increased, in order to widen the selection of different cover levels to consumers. The result of this is that many members have downgraded to lower benefit options for affordability reasons, but it has also meant that their cover levels have reduced.

Graph 3 shows the combined membership of the four largest open medical schemes, categorised by percentage into five cover level descriptions, comparing 2006 with 2020. In 2020, these four schemes represented 82% of the open medical scheme market, so these trends are reflective of overall behaviour.

Graph 3

The benefit downgrades are quite evident – in 2006 almost 45% of families were covered on options considered ‘very comprehensive’ or ‘comprehensive’, whereas by 2020, less than 15% of families were. Conversely, 45% of families in 2006 were covered on the bottom two benefit option categories – ‘restricted cover’ and ‘entry level’ – whereas in 2020, more than 76% of families were.

Other exogenous factors that have influenced private health costs were the conversion of the tax treatment on contributions – from a full tax deduction to the fixed medical tax credit in 2013/14 – and the introduction of VAT on all private medical services in the late 1990s. Medical schemes are not eligible to register for VAT, so any costs that are inclusive of VAT are carried fully by the scheme with no offset.

Health Market Inquiry

The six-year-long Health Market Inquiry (HMI) undertaken by the Competition Commission represents the most comprehensive analysis yet undertaken of the private sector. Not only was the HMI analysis comprehensive but it also engaged stakeholders transparently, with opportunities for them to provide their own input with counter-analysis and perspective.

The result in the 2019 conclusion of the HMI was a blueprint that represents the most informed recommendations of how to enhance efficiency, improve governance and reduce costs within the private sector. It also confirmed what has been so evident to industry stakeholders, that the status quo is unsustainable and does not nearly serve the needs of the wider population.

The HMI findings were also controversially, but appropriately, critical of government’s role in not intervening with more appropriate and improved policies and regulations over the past two decades.

“We have found there has been inadequate stewardship of the private sector with failures that include the Department of Health not using existing legislated powers to manage the private healthcare market, failing to ensure regular reviews as required by law, and failing to hold regulators sufficiently accountable. As a consequence, the private sector is neither efficient nor competitive.”

Final Finding & Recommendations Report, Health Market Inquiry, Sept 2019

It is an irony that the HMI was established on the insistence of previous health minister, Aaron Motsoaledi, with specific notice of his concerns around high costs in the private sector. Yet it is quite clear from the HMI’s final report, as well as the overview of the causes of cost increases outlined above, that part of the private sector’s high costs was brought about by an incomplete regulatory framework within which it has operated now for more than two decades, and a practical absence of introducing, let alone proposing, any improved policies during this time.

Nonetheless, the recommendations of the HMI are now languishing, with zero appetite being shown by regulators or policymakers in considering the proposed changes.

The proposed National Health Insurance (NHI) has taken centre stage of health policy and one of its tenets is to be a monopoly purchaser of care for the country, requiring the relegation of medical schemes to a minor complementary role alongside the NHI. This ‘complementary’ attribute means that medical schemes will not be permitted to cover services that the NHI will cover.

It is also a paradox that the NHI policy process severely lacks technical and feasibility analysis or any meaningful engagement with stakeholders, yet it is favoured over the solutions proposed by the Health Market Inquiry, that was characterised by rigorous data analysis and in-depth engagement with stakeholders.

Whilst it is obvious that the private sector has inherent problems, it remains highly operational, delivering high quality care. The government’s proposal to effectively destroy a functional component of a universal health coverage framework, rather than seeking to incrementally improve on its valid weaknesses, stands as a complete policy outlier globally.

It will also likely fail a legal test of being a reasonable and rational policy stance, especially since it was the government itself that requested the undertaking of the Health Market Inquiry in order to find solutions on how to improve efficiencies and reduce costs in the private sector. It is now completely ignoring them in favour of the NHI.

The views of the writer are not necessarily the views of the Daily Friend or the IRR

If you like what you have just read, support the Daily Friend