Among ‘the three most important concepts for analyzing the capitalist system’, Thomas Piketty places the capital/income ratio, or as he denotes it ‘β’, first. Piketty is the world’s most celebrated socialist economist, quoted in SA’s media as a supporter of the ANC’s ‘new dawn’ take on land.

He is also infrequently but pivotally mentioned in the corridors of power as an outside sage who understands that our South African struggle for economic freedom continues despite political liberation.

For these reasons, it is worth recalling Piketty’s 2015 Mandela Foundation lecture. This was without doubt the crowning speech of Piketty’s career to date, secured on the back of his global hit, Capital in the 21st Century. There, Piketty resurrects Marxist wealth concentration theory on a quantitative approach by explaining that the capital/income ratio gives a numerical ‘measure of how intensely capitalistic the society in question is’. This measure should interest both those who oppose and support capitalistic systems.

Calculating the national capital/income ratio provides the original perspective of providing a macroview of the endurance of private property rights in a particular state. These numbers provide common ground on which those who come from different ideological backgrounds can meet to think about how to drive the economy forward. Piketty’s preoccupation is with sustainability, in particular with the possibility that, after too intense an endurance, private property itself becomes unsustainable.

Historically, the highest capital/income ratios recordedover the long-term have been β = 8 or 9, mostly in aristocratic Europe. In such cases, the amount of total capital, national wealth net of debt, was 8 or 9 times more than income, net of depreciation and foreign flows, generated in a year.

You could think of this as a dam that holds up to nearly ten times more water than flows in (less outflow) every year. The walls of private property in such cases must be extremely high and robust over a long period to contain the vast sum of accumulated wealth.

Individuals and companies have capital/income ratios worth thinking about, too. For someone starting work at R3 500 per month, and who has a mere R3 500 rand in assets, the ratio would be a small fraction, roughly β = 1/12. This ratio will rise over a lifetime on an even savings rate, unless the numerator (accumulated wealth) is somehow depreciated by a force greater than savings. Theft, inflation, and capital depreciation through bad investment in toxic assets are a few examples of what brings down β on an individual level. Naturally, if such depreciations occur on a national scale then β will reduce at that level too.

For whole countries, however, the practical minimum is much higher than 0. The historic national minimum is just above β = 2. This was achieved in Europe after two World Wars (on either side of the Great Depression), which killed more than 150 million and in which 3.5 terawatt hours of explosives were detonated.

For the capital/income ratio to drop any lower would require the entire country to produce more in just two years than has been accumulated to date (since time immemorial) and for practically none of that production itself to translate into newly accumulated wealth. This is both hard to imagine and impossible to find in Piketty’s data, so he describes β = 2 as the economic ‘blank slate’ – the de facto zero starting point from which the process of accumulation begins anew.

From this ‘blank slate’, egalitarian growth comes within grasp. In France, the three decades after 1945 were called trente glorieuses because of the conjunction of rapid GDP growth, average real income increasing by a factor of 5, inequality of both wealth and income compressing, radical poverty reduction and a massively swelling middle class. Piketty’s central point is that, for the ‘thirty glorious years’ after β fell to ‘blank slate’ levels not just in France but everywhere, that data is available.

It is crucial to note that β values are more important than the inequality measurements more commonly quoted from Piketty’s work. In France in 1945, for example, the richest 10% owned more than 75% of total wealth. That is more extreme inequality than SA’s current distribution in which the richest 10% own 68% of total wealth. But the ‘30 glorious years’ that followed were glorious precisely for the poor and middle class and did as much to reduce wealth inequality as the World Wars and the Holocaust did, although by ineffably preferable means.

In short, high-wealth inequality can be vigorously protected through a robust system of property rights, saving lives and value and high growth for the poor and middle class at once. But only if flow is not dominated by past accumulation; only if β is low. Hence Piketty writes in Capital that ‘β does measure the overall importance of capital in a society, so analyzing this ratio is a necessary first step in the study of inequality.’

Piketty’s focus in his Mandela Foundation lecture and in Capital is on the other end of the capital/income scale. In the book, he analyses various concerning effects associated with high β values as, according to his ‘two fundamental laws of capitalism’, β is directly correlated with property owners’ share of capital income (versus labour) and inversely correlated with growth (ceteris but not always realistically paribus). According to his third law, perhaps the most distressing, β is directly correlated with the ‘annual inheritance flow’, which is the rate of money flowing through gifts and inheritances relative to national income.

19th century France hit all three markers on a high β of 7, painting the historic picture. GDP growth slumped to around 1%; income was high for capital owners while wages did not rise with productivity; and annual inheritance flows were about one quarter of βtotal income. Therefore, 80-90% of all French wealth was inherited wealth. If you saw a quality asset in France, nine out of ten times you were looking at an inheritance.

In this world, wealth was not earned, it was bred. As Piketty offered in his Soweto lecture, if there had been a genetic marker (like skin colour or a green dot on the cheek) to distinguish those who were originally wealthy, it would have continued to track wealth almost indefinitely.

Piketty further said that contemporary SA and 19th century France were much the same. The basis of the comparison is that France already had its lethal anti-inheritance revolution (in 1789) and yet kept its high β. So,despite the guillotine and the grand promise of liberté, egalité, fraternité, almost all wealth remained inheritance.

Piketty slammed the 1789 coup d’état from his podium in Soweto as ‘a bourgeois revolution par excellence’. He argued that this revolution did nothing but fool gullible peasants and the urban proletariat into thinking they were free when really they remained shackled by economic rather than political chains. Who denies that this is our lived experience today?

In reference to those contemporaries in 19th century France who denied the need for progressive taxes on the false pretence that ‘we’ve done the French Revolution, we don’t have aristocrats, we are a country of equals’, Piketty’s joke was much appreciated: ‘We can see the elites have a lot of imagination to justify their position’.

Piketty drew the conclusion: ‘It’s only very violent shocks which occurred in the 20th century which finally convinced the elite to accept a number of fiscal and social reforms that were not adopted before. I think this is of interest to South Africa…’

Violence being of interest to SA brings one to the 2019 front-page headline: ‘Crime: We are under siege’, and the data showing that 21 022 people were murdered in the country in 2018, representing a 39% increase in murders since 2011/2012, and that murders had risen by 3.4% since President Cyril Ramaphosa took charge. The connection to property rights emerged in a pie chart labelled ‘armed robbery on the rise in SA’, with over 1 100 truck hijackings, 16 000 business robberies, 20 000 house robberies, 22 500 car hijackings (up from 16 500) and 80 000 street robberies, suggesting an image of the business end of a Kalashnikov trained on capital itself.

Crime reporting and financial journalism usually appear on different pages, if not in different publications. But the Pikettian view understands violence in the context of wealth inequality and this view defines the mainstream conviction that masses of accumulated wealth walled into a few hands results in a dystopian SA where elites must either dismantle the walls of private property voluntarily, or face the irresistible force of socio-economic history – or, as Piketty puts it, a ‘proletarian revolution and general expropriation’.

On this view, taxing income will never be enough. The problem is not wealth flows, which are already progressively taxed to the Laffer curve’s zenith in SA. Rather the problem is the extent to which stock dominates flow, the high capital/income ratio. A major difference between South Africa’s progressive tax regime and economic conditions of 19th Century France is precisely the significance of the already dominant accumulation under apartheid.

On this point, Piketty cannot be contradicted. No country with South Africa’s level of wealth inequality and a high β has ever survived. By every precedent, the dam will fall after one million separate hammer blows (already half a million people have been killed since our last revolution) or through the coordination of revolutionary violence into one concentrated blast. If, as the ANC offers, wealth will be ‘reallocated’ in an orderly fashion ‘by the book’, this would be unprecedented. And mercifully so.

SA’s ‘new dawn’ to date is a new dawn for Piketty’s anti-private property view. Consider Ramaphosa’s Desmond Tutu ‘Peace Lecture’ in October 2018 where he explained the country’s record levels of violence in Pikettian terms. Until the ‘historic injustice of accumulation’ had been ‘corrected’, Ramaphosa said, ‘we will not be able to realize a lasting peace’. That is the theory, and, for the practice, refer to the new dawn signature policies: expropriation without compensation, National Health Insurance, the Credit Act, and the new ‘debate’ on prescribed assets. All these aim to ‘correct’ or ‘share’ accumulated wealth by dismantling parts of the property wall directly.

Piketty’s comparing the French Revolution of 1789 and SA’s revolution of 1994 – both loudly promising political freedom but failing to deliver economic freedom – could not be more popular in the Union Buildings. And yet in one sense Piketty’s views are clearly at odds with Ramaphosa’s. Piketty wrote in Capital that ‘analyzing this ratio [β] is a necessary first step in the study of inequality.’ But neither Ramaphosa nor any of his staff have ever publicly taken this step, and the capital/income ratio remains almost totally unknown.

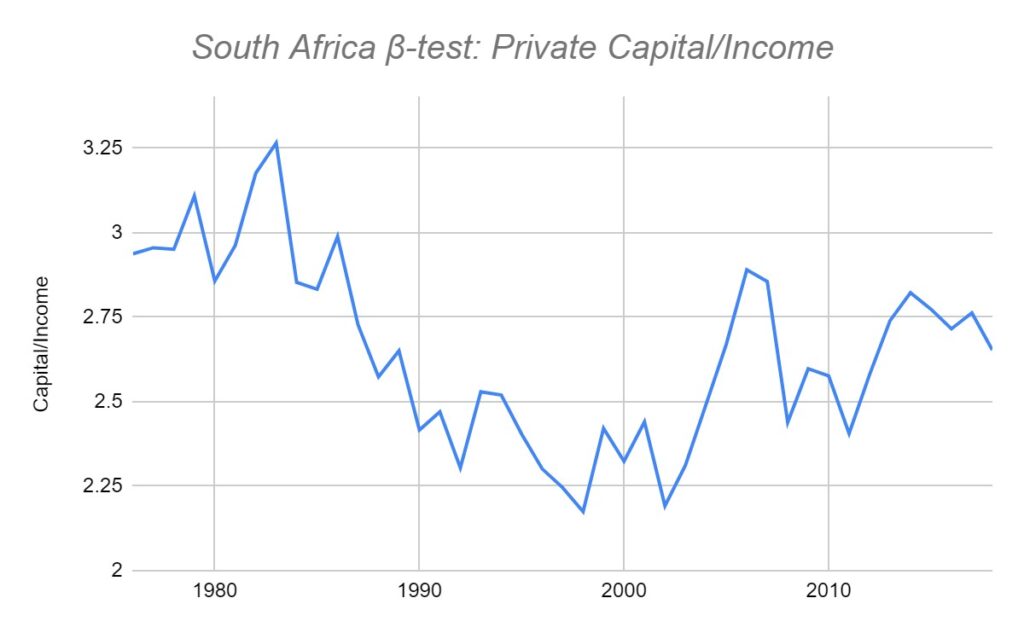

Quite as startling, Piketty himself always produces this calculation for countries under his analysis, except in SA’s case. Perhaps that is because, in SA, β = 2.5.

To follow the arithmetic, consider that the South African Reserve Bank estimates net wealth at R10.8 trillion (as of 2016) and Stats SA derived net national income value of R4.4 trillion at that time. 10.8/4.4 = β = 2.45.

As a caveat, state wealth is not included in this calculation, nor in many of Piketty’s β computations, since only private wealth accumulation is relevant to measuring the strength of private property rights. State assets are also difficult to value. Still, adding state wealth and then netting its debt would possibly bring SA’s β value down even further since our public debt is now greater than net national income.

A knee-jerk assumption to make is that this β value is so low simply because of recent capital flight from socialism’s new dawn in SA. But economists Gavin Chait and Anna Ortoffer made similar, independent capital/income findings in the late Zuma-era. The following graph deliberately uses assumptions that produce the highest capital/income ratios of the three.

To find common ground on the existential debate on property rights, proponents must publicly recognize the common knowledge that in some circumstances an accumulation may be justly and violently destroyed. The US Civil War would be such a case. But, likewise, in certain circumstances attacks on private property cannot and must not be tolerated, for they amount to abuse pretending to be virtue.

Here is Piketty himself comparing a β = 7 19th century Europe to a β = 3.5 19th century USA, especially its northern ‘free states’:

‘[T]he low capital/income ratio in America reflected a fundamental difference in the structure of social inequalities compared with Europe. The fact that total wealth amounted to barely three years of national income in the United States compared with more than seven in Europe signified in a very concrete way that the influence of landlords and accumulated wealth was less important in the New World. With a few years of work, the new arrivals were able to close the initial gap between themselves and their wealthier predecessors—or at any rate it was possible to close the wealth gap more rapidly than in Europe.’

When Ramaphosa says ‘until the wealth is shared among the people and the land is shared among all who work it – we will not realise lasting peace’, he not only fails to realize ‘the land’ is now less than 1% of wealth stock and so offers no ‘radical’ redistribution whatsoever. He also fails to appreciate that ‘new arrivals’ are ‘able to close the initial gap between themselves and their wealthier predecessors’ more easily here than almost anywhere else in history.

SA’s socio-economy is at ‘blank state’ economic status now, too. There is a season to burn the grass to ash and a season to plant, but SA’s time is out of joint. Its leadership, with great ‘imagination’ and no quantitative thrust, continues to ‘woke’ up in 19th Century France.

[Picture: Sue Gardner, https://commons.wikimedia.org/w/index.php?curid=32385741]

If you like what you have just read, become a Friend of the IRR if you aren’t already one by SMSing your name to 32823 or clicking here. Each SMS costs R1.’ Terms & Conditions Apply.