India bought some oil for rupees, sparking headlines that say the end of the dollar is nigh. It isn’t.

BRICS, no matter its composition, will never dethrone the mighty dollar. Nor will any other grouping of ‘Global South’ countries.

Last month, shortly before the 15th Summit of the Brazil, Russia, India, China, and South Africa economic alliance (BRICS) convened here in this country, India announced that it had bought a million barrels of oil from the United Arab Emirates (UAE), and paid in rupees for the first time.

This follows a bilateral agreement, concluded on 15 July, that permits the use of rupees and dirhams, instead of dollars, for bilateral trade settlements between India and the UAE.

The oil transaction, according to Reuters, came after another deal involving the sale of 25kg gold from a UAE gold exporter to a buyer in India at about 128.4 million rupees ($1.54 million).

BusinessInsider declared it to be ‘one step further’ in ‘the dedollarisation trend’.

An article by Bethany Moorcraft, writing for MoneyWise, was a little more hedged: ‘Dollar dumped? The UAE to join India in BRICS bloc after the two powerhouses trade 1 million barrels of oil for rupees instead of USD for the first time — what this means for the greenback.’

She pointed out that while dedollarisation might be a popular idea among BRICS countries, US Treasury Secretary Janet Yellen asserted that no currency exists today that could replace the dollar.

Moorcraft’s story was republished, however, by Yahoo! Finance and by Microsoft’s MSN, however, both of which gave it a far more sensational treatment.

Yahoo! went with, ‘Dollar dumped? … why this could be the start of the end for the greenback’.

MSN, along similar lines, ran with the headline, ‘Is the dollar being dethroned? … why this could spell doom for the greenback’.

‘Dollar demise,’ screamed the alarmingly popular quackery-turned-alt-right-conspiracy website Natural News. ‘The days of U.S. dollar dominance in global trade are numbered.’

The pseudonymous Tyler Durden, at ZeroHedge, another crackpot website which like a stopped clock is correct twice a day, called it, ‘Another blow to the petrodollar,’ warning that ‘dedollarisation would drastically diminish US economic power and wreck the country’s economy’.

Begged to differ

India’s oil and gas minister, Hardeep Singh Puri, begged to differ with all these shrill predictors of the dollar’s doom.

Admitting that he ‘would like to be able to transact everything in rupees’, he also said that the US dollar will remain the currency of choice for transactions in international oil markets, that dollar dominance will remain, and that dedollarisation is still far away.

A common-sense analysis of the situation confirms that Puri is correct.

It makes no sense for any country to accept payment for its exports in, say, Indian rupees, beyond what it needs to pay for imports from India.

A bilateral local currency settlement agreement, such as that between India and the UAE, is not likely to be applied to anything beyond the lower of the trade volume in either direction between the countries.

The UAE is reportedly keen to increase its bilateral trade with India, in particular to secure its food supply chain. It is investing heavily in so-called ‘food parks’ in India. It can therefore use rupees to pay for food and other imports from India.

If the UAE decides to pay for imports from the European Union or Japan in rupees, we may have a more interesting situation on our hands. Until then, fluctuations in how much international trade is conducted in dollars pose no threat to that currency’s global status as a reserve currency.

Everyone accepts dollars, and dollars are backed by a large country with a reliably productive citizenry and a government that is well able to tax them. About 56% of the reserves held by the world’s central banks are dollar-denominated. That isn’t going to change any time soon.

Hegemony

To fans of BRICS, this ‘hegemony’ is perceived to be a problem. They believe that it gives the US some sort of imperial power over the rest of the world.

Economist and blogger, Noah Smith, has written an excellent assessment of whether the very concept of BRICS even matters.

He says it doesn’t, and I believe he is right.

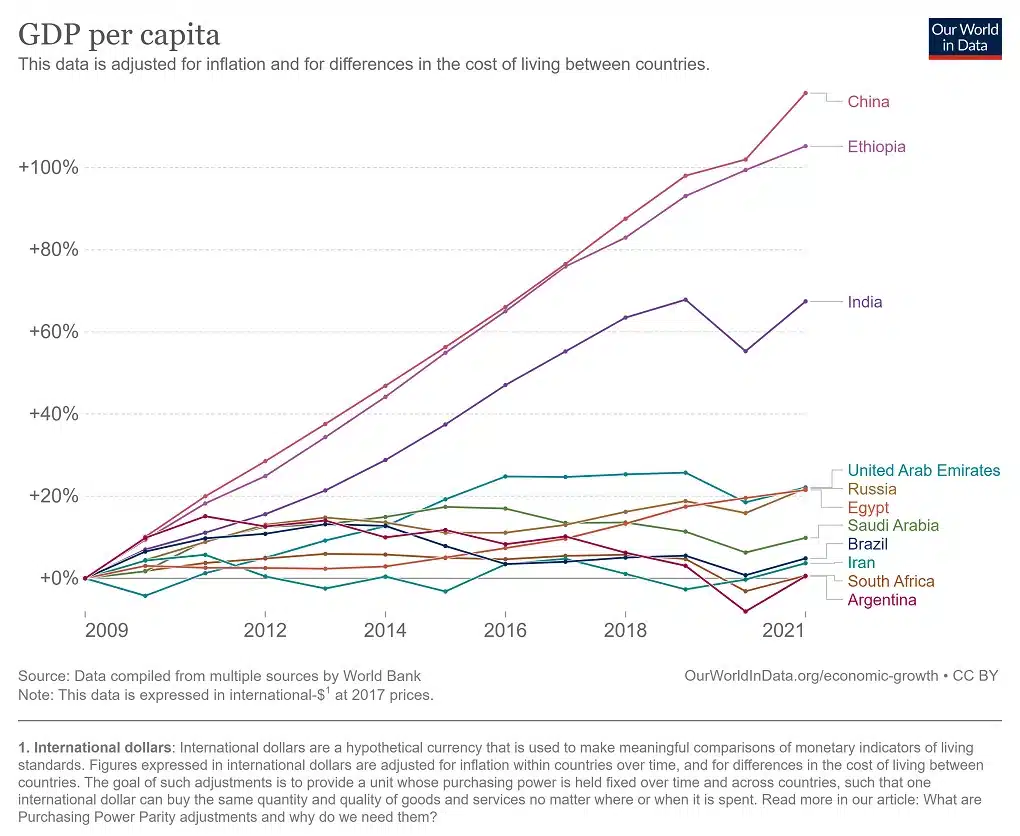

Without any accession criteria or procedures, BRICS on a whim decided to include Saudi Arabia, Iran, UAE, Argentina, Egypt, and Ethiopia.

Of those, only Ethiopia has significantly increased its GDP per capita (at purchasing power parity in constant 2017 international dollars) at an appreciable pace since 2009, as did China and India.

Smith offered this illustration:

All the other members of the expanded BRICS have grown by no more than 20% in that time, reflecting an annual growth rate of a mere 1.5%.

South Africa and Argentina have not grown at all during that time.

In 2008, South Africa’s GDP per capita stood at $13 596. In 2022, it was lower, at $13 470. It might as well quit calling itself a ‘developing country’. It isn’t developing at all.

BRICS member countries are extremely diverse, with vastly divergent interests. They are often at odds with each other. From massive ‘anti-dumping’ duties on each other’s exports, to high-handed claims to each others’ territory, the grouping is far from the stable, peaceful, free-trading economic bloc it pretends to be.

Anti-Western

Smith listed a litany of reasons why BRICS is not, and will never be, the anti-Western hegemon that it aspires to be.

The de facto leader of the BRICS countries, China, is surprisingly unpopular among India, Brazil, and South Africa, he points out, and tensions between BRICS member countries are often quite volatile.

India, for example, has banned many Chinese mobile apps, as well as some Chinese imports, while it is strengthening its economic and strategic ties to the US.

Countries that are frequently at odds will never, Smith argues, create a common currency, which Russia in particular has floated.

BRICS, for its part, hasn’t actually done anything. The New Development Bank (NDB), a rival to the World Bank launched with great fanfare in 2014, has achieved very little, disbursing less than $1 billion in loans to date.

By comparison, dollar-denominated debt outside the US continues to rise, with levels reaching $13.4 trillion as of mid-2022.

The BRICS Contingent Reserve Arrangement, which is meant to supplant the International Monetary Fund (IMF), has also done effectively nothing.

And, Smith adds, the system of undersea fibre-optic cables that BRICS promised to lay have not materialised.

Rounded to the nearest billion dollars, BRICS has done absolutely nothing. Despite this, people talk about it as if it is not only an important organisation of global significance, but an active threat to the hegemony of Western financial institutions and the dollar as a reserve currency in global trade.

It is nothing of the sort.

Common currency

Even if BRICS were to achieve the impossible, and create a common currency, it won’t dethrone the dollar. The far stronger European Union created a common currency, and it didn’t dethrone the dollar, either.

Smith also points out that contrary to BRICS propaganda, the World Bank and IMF don’t have a monopoly on emerging-market lending. China itself does plenty of intra-government lending as well as international project finance.

‘So there’s really not much to the supposed Western or US control of the global financial system — meaning there’s just not much for BRICS to replace in the first place,’ Smith writes. ‘The outsized role the US plays in the system exists primarily because of convenience, not hegemony; to see this, witness how the BRICS New Development Bank does most of its borrowing in dollars. It’s not because the U.S. makes them do it; it’s just easier.’

As I once warned, the largest economy in BRICS by a considerable margin, China, more than twice as big as its nearest rival, India, is slowing at an alarming pace as its profligate public spending, its declining population, and oceans of bad debt catch up with it.

The notion that any or all of the BRICS countries, even if that grouping were to expand to represent more of the so-called ‘Global South’, will soon be able to ‘dethrone the dollar’, is absurd. It is a fever dream of the leaders of poorly governed, mostly autocratic nations.

Blueprint

If these countries really do want to rival the liberal democracies of the West in terms of economic power, they would do far better to download the Fraser Institute’s Economic Freedom of the World Report, and consider its assessment criteria a blueprint for achieving both economic growth and improved living conditions for the poor.

The Fraser Institute report ranks countries on dozens of criteria in five broad areas, namely size of government, legal system and property rights, sound money, freedom to trade internationally, and regulation.

It shows that there is a strong correlation between a country’s economic freedom rating and its GDP per capita, as well as many other indicators of well-being, such as lower poverty rates, better life expectancy and higher gender equality.

South Africa ranks 99th out of 165 countries they assessed, which places it in the middle of the third quartile.

Of the traditional BRICS countries, only India and Russia rank slightly (but not significantly) higher, at 89th and 94th respectively. Brazil ranks 114th, and China, from whom the South African government is perversely taking economic policy tips, ranks 116th. None feature in the top half of the economic freedom index.

The new kids on the bloc, Saudi Arabia, Iran, UAE, Argentina, Egypt, and Ethiopia, aren’t any better. They rank 86th, 159th, 49th, 161st, 150th, and 151st, respectively.

Only the UAE makes it into the top half, and four of those are fighting Zimbabwe, Sudan, and Venezuela for the title of worst in the world.

All these government need to do is take those Fraser Institute criteria and implement policy reforms that will improve their scores in all, or at least most, of them. If they diligently keep doing that, then rising GDP per capita, lower poverty rates, and growing global economic power will inevitably follow.

Succeed they will, but still, they won’t topple the dollar as a global reserve currency. The dollar is just too convenient for that.

Image: A Kremlin publicity photograph of a lonely Russian president Vladimir Putin, attending the 15th BRICS Summit in Johannesburg via video link.

The views of the writer are not necessarily the views of the Daily Friend or the IRR

If you like what you have just read, support the Daily Friend