Now that the excitement – (or lack thereof; see South African Voter Turnout Slumps in Municipal Elections) – of the local government elections has subsided, it’s a good time to turn our attention to South Africa’s overall fortunes for the coming months.

Will more coalition governance be better for creating environments for investment and job creation? Some municipalities probably have better skills, finances, and capabilities than others – Cape Town immediately comes to mind.

Unfortunately for others, such as those in the Eastern Cape and North West, the continued downward trend is likely to continue. Just recently media reports indicated that Supreme Poultry was looking to move its operations away from Mahikeng, potentially following in the footsteps of Clover, which announced in June this year that it would close its cheese factory in Lichtenburg. They cited poor service delivery as a reason for moving.

The flow of capital

There is no moral duty on a business or an investor to sink time and capital into a given area – to ‘give’ jobs as such. Capital will flow along the path of least resistance, and it’s up to governments to ensure they place as few barriers as possible across the path of business growth and job creation. Politicians and bureaucrats are of course free to wail on when a business chooses to move away, but ultimately, they only have themselves to blame.

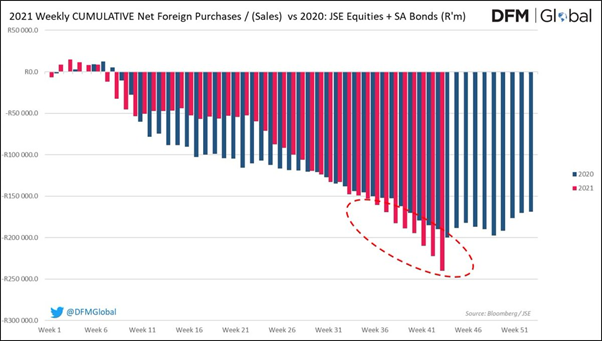

This graphic indicates the extent to which foreigners have been selling off the JSE equities and South African bonds they had. The trend has picked up considerably this year as compared with 2020. No doubt the violence and looting earlier in the year, and enduring rolling blackouts (as well as pretty much glacial ‘structural reform’), have sent all the signals that potential investors may need.

Something that is often lost in analyses of South Africa’s economic decline is even an acknowledgement – never mind actual discussion of – the fundamental role that ideology and philosophy play in the formation and implementation of government ideas and policies. The consequences, good or bad, are downstream from policies, and policies are downstream from ideology. This is to say, if a politician or bureaucrat starts from a position that the state should be in control of and managing the economy and people’s lives, one shouldn’t be surprised when they pursue policies that will inhibit and suffocate private enterprise and always stifle the growth of a liberal, robust, free society.

It falls on local and foreign investors and businesses, communities, and families to do their due diligence and not be swayed by grand rhetoric at investment summits and the like. The reality on the ground should be of paramount importance for potential investment decisions. Rolling blackouts continue to seriously hinder any growth potential, and government is looking at potentially more stringent B-BBEE regulations in 2022.

In his 2021 Medium Term Budget Policy Statement, Finance Minister Enoch Godongwana largely stuck to script – which is to say, more of the same, and nothing of the kind of truly radical reform that is needed to unlock the growth rate the country needs. He struck a tone of fiscal consolidation, and while many will consider that a ‘win,’ the Statement didn’t contain anything of note that would get the economy moving in any substantive way. The growth rate is forecast at 1.8% in 2022, and 1.6% in 2023; South Africa’s emerging market fellows are expected to grow at an average of 5% in the short-term.

Godongwana indicated that state-owned entities’ requests for bailouts will be resisted. Only time will tell whether he and others in government can resist that pressure; the same goes for public sector wage increases. He also kicked into touch mounting calls for a Basic Income Grant. Radical, pro-growth reform may come along at the time of the 2024 general elections – for now, government appears happy to stay with the middling, low-growth and low-investment path.

Risk appetite

This may sound slightly pithy – and it doesn’t always work out in this manner, because nothing in investing is strictly linear – but given all the risks involved in the South African investment space, one can argue that the potential upsides are massive, presuming, of course, that the country heads in some kind of pro-growth structural reform direction over the next decade. For those international investors with a large appetite for risk, South African companies and stocks offer great value – but it’s up to each one to decide just how long their patience for notable returns will last.

For local investors the same rationale applies, as long as one doesn’t put all one’s eggs in a rand-denominated basket. The rand has been riding a massive commodities boom over the last few months – the wave will eventually crest and then decline. With that will come a weaker currency, and further pressure will be placed on government’s finances; especially if it doesn’t keep some kind of lid on massive spending plans.

South African mining and agricultural industries have been performing very well, especially compared to last year, but in all probability the peak is actually already behind us. No investment path will deliver perfect returns, but it would be best for people to build some measure of a diversified portfolio, with local and foreign exposure. Ultimately, you should presume that the worst possible political policy scenario will play out – will you be state-proof enough to survive?

Given that so many citizens have become rightly fed up with government as a whole, and in light of some apparent new impetus in local government, those politicians, bureaucrats, and policymakers who truly desire a better space for South Africans would be well served by letting go of their tendency towards central planning – and the hubris and devastating consequences that always accompany such an approach.

The views of the writer are not necessarily the views of the Daily Friend or the IRR

If you like what you have just read, support the Daily Friend