The run on Silicon Valley Bank (SVB), which scuppered it, could be the first of many, as regulators and central banks fuel the panic. It’s all chickens coming home to roost.

Regulators always seem surprised when, in the words of Robert Southey, their chickens come home to roost.

Silicon Valley Bank was an institution in the technology sector. It was founded in 1983, and has done business with much of the tech sector based in San Francisco, and later, elsewhere. It grew with the sector and became a major bank, offering full service to Silicon Valley tech entrepreneurs, from transactional accounts to business loans to investment products.

It had a fatal flaw, however. In its mission to be more hip, more woke, more trendy and more with-it than any other bank, it forgot about the basic business of banking. In particular, it neglected its risk management. It put almost all its eggs in a single basket, namely long-term (10- and 30-year) US Treasury Bonds, and those bonds were under water.

When governments print money, that money first gravitates towards assets, such as houses and stocks, inflating economic bubbles. Those bubbles in due course burst, as bubbles must.

The tech sector was one of the major beneficiaries of the quantitative easing and cheap money that flooded the market in the wake of the 2008 financial crisis. It started a very long bull market almost immediately.

That bull market turned into outright mania when the pandemic came around in 2020 and boosted demand for technology services aimed at working from home and replacing in-person meetings with video conferencing. SVB, flush with tech sector deposits, boomed with it.

At the end of 2021, however, the bubble burst. The tech stock market has lost about a third of its value since then. And SVB deposits went down accordingly.

Bank run

Last week, SVB reported that it had sold $21 billion worth of US Treasury Bonds at a loss of $1.8 billion. It sought to raise an additional $2.25 billion in new equity to bolster its liquidity. The next day, the bank’s stock fell sharply. Depositors panicked, withdrawing about 40% of the funds the bank had on deposit. Bank run. Game over.

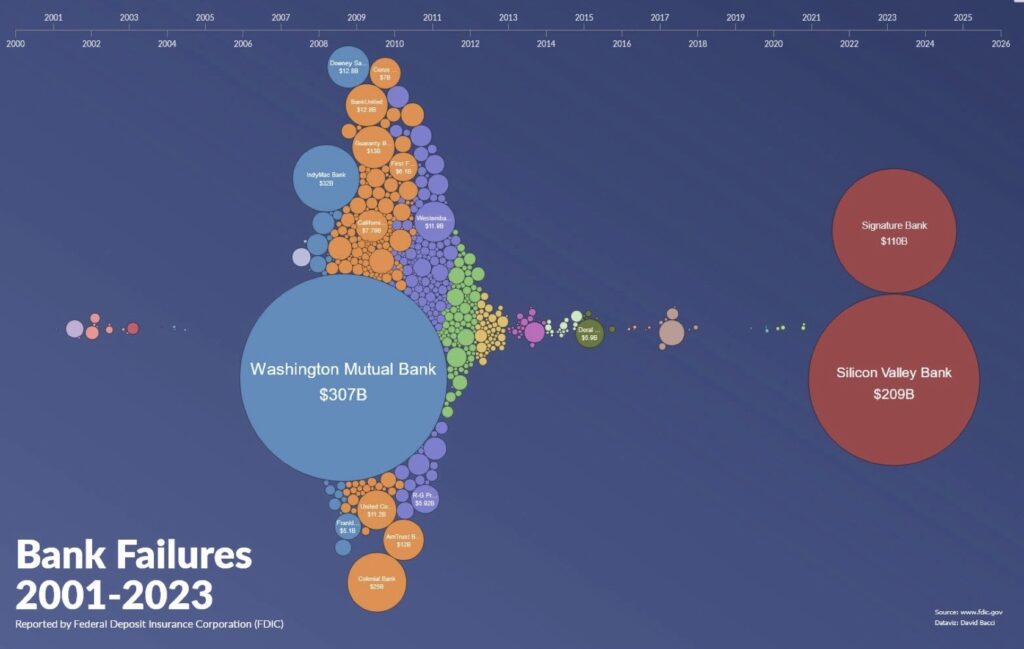

On Friday 10 March 2023, SVB, with $209 billion in assets, was closed. The Federal Deposit Insurance Corporation (FDIC), a statutory body created to protect bank depositors by insuring their deposits up to a limit of $250 000, housed its assets in a new bank.

On Sunday 12 March, Signature Bank of New York followed, and was likewise taken over by the FDIC. It was just over half the size of SVB, at $110 billion.

These banks are huge. SVB was the 16th-largest bank in the United States.

Even adjusted for inflation, the only larger US bank that failed during the 2008 global financial crisis was Washington Mutual, with assets of $307 billion (which would be worth $429 billion today).

In a free-market capitalist world, which people mistakenly believe we live in, that would have been that. Small depositors are protected by a deposit insurance scheme on the presumption that they aren’t capable of evaluating the financial soundness of a bank, while big depositors along with investors are wiped out.

After all, one of the great virtues of free market capitalism is not only that it incentivises success with profit, but also that it rapidly punishes failure, so that the capital misallocated to bad businesses can be redirected towards more profitable, sustainable ventures.

But we don’t live in a free market capitalist world; at least, not where banks are concerned. Banks enjoy a special status, and are incentivised to take extraordinary risks by the simple mechanism that they are unlikely to have to face the consequences of failure.

‘Don’t Panic’

The FDIC, the US Department of the Treasury, and the Federal Reserve hurriedly issued a joint statement that said ‘Don’t Panic’, in large, friendly letters.

In an unprecedented move, the FDIC announced on Monday that it would protect depositors in SVB and Signature Banks not only up to $250 000, but that it would cover 100% of deposits. It promptly set up ‘bridge banks’ that would enable customers to conduct unrestricted business as usual.

The Federal Reserve has already an emergency loan programme, which bankers at J.P. Morgan expect will pump $2 trillion of liquidity into the US banking system.

Of course, unprecedented moves to prop up the banking system do not signal ‘Don’t Panic’. They signal ‘Panic Fast and Panic First’.

The FDIC’s commitment to cushion even large depositors means that those who chose their banks with more prudence are getting fleeced to protect depositors who didn’t do their due diligence on their banks.

When the government always rides to the rescue, this creates what economists call ‘moral hazard’. By protecting people from the consequences of their failures, you are incentivising exactly the sorts of risk they should not be taking.

The risks that took down SVB and Signature are not isolated. All banks now operate in an environment where inflation is high, interest rates are rising, and economies are slowing down. House prices have been on a decade-long boom fueled by easy money too, and like other asset bubbles, it is showing signs of popping.

Bad apple

The grim economic outlook will put all banks under pressure.

Credit Suisse, a bulge bracket bank founded in 1856, managing CHF530 billion ($574 billion) in assets, has been wobbly for years, but is now closer than ever to hitting the wall.

Its stock hit all-time lows this week, trading more than 96% below its post-2008 high. After reporting concerns about accounting irregularities, it high-tailed it to the Swiss National Bank to borrow $54 billion to keep it afloat.

Its problems are different from those of the US banks that failed last week, but it is also a far bigger systemic risk to the global economy. Unlike SVB and Signature, it presents a real risk of global contagion.

Worldwide, central banks and regulators will be stepping up to save weak banks, badly managed banks, and banks that took on too much risk. And so the cycle repeats itself.

Told you so

Free market advocates have long warned that easy money and the practice of using monetary policy to ameliorate economic downturns only extends those downturns, and fuels future booms that, inevitably, go bust.

Witness libertarian Ron Paul’s memorable speech to Congress in 2001, in which he predicted in extraordinary detail how the 2008 housing market collapse and global financial crisis would unfold.

Nothing has changed. Governments the world over are still incentivising banks to issue high-risk mortgages in pursuit of ‘affordable housing’. They are still reacting to economic downturns by running the money printing press. They are still treating banks as ‘too big to fail’.

Despite banks being perhaps the single most heavily-regulated industry on the planet, governments blame a lack of regulation for bank failures, as if the failure of bad banks ought to be prevented, and as if banking regulation could have prevented the financial crises caused by the collapse of asset bubbles inflated by easy monetary policy.

Free marketeers have been predicting financial crises for decades, and have been saying ‘told you so’ since at least 2008. Nobody listened.

Well, here we are again. Insane amounts of money were pumped into the system, blowing up first asset price bubbles and then general price inflation, which inevitably led to an economic crisis, with banks starting to collapse.

Gold is trading near its all-time high, and bitcoin has gained 50% in the last few months. Investors are seeking safe havens, and there aren’t many around.

Wild ride

Don’t get me wrong: this correction is necessary. We cannot keep living in a dream world funded by printed money, no matter what the Magic Money Tree Theory people would have you believe.

The chickens must come home to roost, but the experience will not be pleasant, for any of us.

Will this crash be bigger than 2008? We’ll have to wait and see.

Will governments learn from it? Of course not. They never do, because it would spell the end of deficit spending.

It would also end the illusion that governments can, using the single variable of central bank interest rates, control the fate of their economies. Government-employed economy emperors don’t like to be exposed as naked.

So, buckle up. It’s going to be another wild ride.

The views of the writer are not necessarily the views of the Daily Friend or the IRR.

If you like what you have just read, support the Daily Friend.