Most of us spend our entire lives using money every day. We earn it, we save it, we worry about it, we plan around it – and yet we rarely stop to ask a surprisingly basic question: What is money, really?

We tend to think we know the answer. Money is rands, or dollars, or numbers in a bank account. It is something issued by governments and managed by central banks. It feels familiar, almost natural, like it has always existed in its current form.

But historically, that is not true at all.

For most of human history, money was not designed by governments or economists. It emerged gradually, through trial and error, as societies searched for reliable ways to store value and trade with one another across time and distance.

Different things have served as money at different times, including shells, salt, beads, silver, and eventually gold. And what is striking is that across cultures and centuries, societies kept converging on forms of money that shared one particular characteristic: they were difficult to create.

That turns out not to be an accident: because whenever money becomes easy to produce, more of it eventually gets produced. When that happens, its ability to store value begins to erode. This pattern repeats again and again throughout history, from ancient coin clipping to modern inflation.

One way to think about money is therefore not as a political invention, but as a kind of tool: a social technology for storing economic value across time.

Like any technology, money evolves, and this is where the modern world introduced a new problem.

In the digital age, we learned how to copy information perfectly and instantly. You can duplicate a file, a photo, or a document at almost zero cost. But that creates a paradox: if digital things can be copied infinitely, how can digital money ever be scarce?

For decades, the answer seemed to be that it couldn’t. Digital payments required trusted intermediaries such as banks, card networks, and payment companies to maintain a central ledger and prevent cheating.

Then, in 2009, something new appeared: Bitcoin.

Bitcoin is an attempt to solve the problem of how to create a digital currency that resists cheating and inflation. It does this by anchoring it in something that cannot be faked: the expenditure of real-world energy.

In this session, I will explain why that idea emerged, how it works, and what problems it is trying to solve – not always perfectly.

What is money?

Let us go back to that basic question: what is money?

Economics textbooks usually answer that question by describing the three main functions of money: money is a medium of exchange, a store of value, and a unit of account. That definition is useful, but it doesn’t really explain why certain things become money and others don’t.

To understand that it helps to step back and imagine a world before money existed. In early societies, people traded directly: they bartered. You might barter grain for tools, livestock for clothing, or fish for beautiful jewelry.

But barter has an obvious problem: both parties have to want exactly what the other person has at the same time. Economists call this the “double coincidence of wants,” and it makes large, complex economies almost impossible.

To solve that problem, societies began adopting widely accepted goods that people would take even if they didn’t need them immediately – because they trusted someone else would accept them later. In other words, goods that were easy to trade became money.

This process was not centrally planned. Nobody held a conference and voted for gold or silver. Money emerged through competition. Different goods were tried, and over time some worked better than others.

Across history, we see a surprisingly consistent pattern. Many things were used as money: shells in Africa and Asia, beads in North America, salt in parts of the Roman world, livestock in pastoral societies. But most of them eventually failed.

Figure 1 – Kijik trade beads from Alaska. Image source: https://home.nps.gov/lacl/blogs/january-2014-beauty-and-the-bead.htm

Why? Because once something becomes widely accepted as money, there is a powerful incentive to produce more of it.

If shells are money, people start collecting shells. If beads are money, someone figures out how to manufacture beads more efficiently. The moment supply expands too easily, the value of that money begins to fall, and societies gradually abandon it.

Over centuries, this evolutionary process pushed humanity toward forms of money that were increasingly difficult to produce. Silver lasted longer than shells. Gold lasted longer than silver. These things were valuable not because governments declared them valuable, but because nature imposed limits on their supply. Gold is rare, difficult to extract, and requires significant effort and resources to mine. No matter how strong demand became, new supply could only increase slowly.

This turns out to be the key insight: Good money is hard to create. Or, put differently, money works best when nobody can suddenly make a lot more of it.

When people trust that the supply cannot easily expand, they are willing to save in it. And when people are willing to save, economic coordination across time becomes possible: investment, long-term planning, contracts, pensions, civilisation itself.

Money is more than a payment tool. It is a mechanism for storing human effort across time. You can think of it as a bridge between the present and the future, a way of preserving the value of work today so that it can be used tomorrow.

Throughout history, societies repeatedly discovered the same lesson: the stronger that bridge is, the more stable economic life becomes. This historical pattern – the search for money that cannot be easily debased – is what eventually led humanity to gold. But gold, as successful as it was for thousands of years, came with limitations that became increasingly visible in the modern world. Those limitations set the stage for the monetary system we live in today, and ultimately for Bitcoin.

The recurring problem: debasement

If money tends to evolve toward things that are hard to produce, history also shows something equally important: Monetary systems repeatedly break when that hardness disappears.

Often, the cause isn’t greed or bad intentions. It is technology. Throughout history, forms of money have lost their value when someone discovered a faster or cheaper way to produce what had previously been scarce.

One striking example comes from early encounters between European traders and societies in Africa and the Americas. In many regions, glass beads functioned as money. They were valued because they were rare, required a lot of effort to make, and were widely desired for ornamentation and trade.

But European manufacturers possessed advanced glassmaking techniques. They could produce beads in enormous quantities at very low cost. What had once been scarce suddenly became abundant. Gradually, as more beads entered circulation, their purchasing power fell. Something that had reliably stored value stopped doing so, simply because production technology had changed.

The same pattern appears elsewhere. In parts of North America, wampum – carefully crafted shell beads – served as money for long periods. When industrial production methods allowed settlers to manufacture large quantities quickly, the supply expanded dramatically and its monetary role deteriorated.

Figure 2 – Wabanaki wampum belts. Image source: https://picryl.com/media/wabanaki-wampum-belts-08066b

Even commodities tied closely to daily life followed this pattern. Salt functioned as money in various ancient societies precisely because it was difficult to obtain and transport. But improvements in mining and transportation steadily reduced its scarcity and undermined its usefulness as a store of value.

The lesson is the same, again and again: money fails when it becomes easy to make more of it. Sometimes technology causes this, as the examples above show. At other times, politics does.

Rulers throughout history discovered another path to the same outcome: altering the money itself. In the Roman Empire, silver coins were gradually diluted with cheaper metals while still being declared the same denomination. Medieval kings clipped coins or reduced precious metal content to stretch government finances. Modern leaders printed vast amounts of paper money, eroding the value of existing money savings. The short-term benefit was obvious – it gave them more money to spend – but the long-term effect was devastating: prices rose, trust in the currency eroded, and new monetary systems eventually replaced the debased ones.

Seen this way, debasement is not an anomaly. It is almost a law of monetary history. Whenever money can be produced more cheaply than before, whether by technological innovation or political decision, it becomes less scarce, and this erodes its reliability as a store of value.

This helps explain why gold eventually became dominant. The advantage of gold was not beauty or tradition. It was that, for thousands of years, no technological breakthrough made it dramatically easier to produce. Then as now, mining requires real physical effort, and even major gold discoveries increase supply only gradually. Nature itself enforces discipline.

But as economies became global and increasingly digital, even gold began to encounter practical limitations, especially when money needed to move quickly across continents and financial systems. Solving those limitations, while preserving scarcity, turned out to be one of the central monetary challenges of the modern era.

Why gold worked: scarcity, stock-to-flow – and its limits

By this point in history, societies had learned something important through centuries of trial and error: money works best when its supply cannot easily expand.

Gold turned out to be unusually good at this. One useful way to understand why is through a concept sometimes called the stock-to-flow ratio. The name sounds technical, but the idea is simple: the stock is the total amount of something that already exists. The flow is how much new supply is produced each year.

For most commodities, production can increase quickly when demand rises. If the price of oil goes up, companies drill more wells. If wheat becomes more valuable, farmers plant more wheat. Supply responds relatively quickly.

But gold behaves differently. Almost all the gold ever mined in human history still exists today, sitting in vaults, jewellery, or central bank reserves. The annual production of new gold is tiny compared to that enormous existing stock: usually only one or two percent per year.

That means even if the price of gold doubles, miners cannot suddenly flood the market with new supply. Production increases slowly, over years, not months, and this stability is exactly what made gold reliable as money. Gold didn’t become valuable because people decided it should be money. It became money because its physical properties made it resistant to sudden inflation. Nature limited how quickly humans could create more of it. In a sense, gold imposed monetary discipline not through laws, but through physics.

But gold was never perfect. As economies expanded and trade became global, the physical nature of gold began to create problems.

First, gold is difficult to verify. Determining whether something is real gold, and whether it is pure, requires specialised testing. Throughout history, people worried about counterfeit coins, alloyed metals, or shaved edges. Trust often depended on institutions or experts rather than simple verification by ordinary individuals.

Second, gold is slow and cumbersome to move. Transporting large amounts across long distances requires ships, trucks, security, and time. Settlement between countries could take weeks or months.

And third, gold is expensive to secure. Storing it safely requires vaults, guards, insurance, and infrastructure, whether it is sitting still or being transported. The very property that made gold valuable – its physical scarcity – also made it costly to handle.

Over time, these limitations led societies to adopt paper claims and later digital claims representing gold, rather than moving the metal itself. Banks and financial institutions became custodians, maintaining ledgers that tracked ownership while the gold remained stored elsewhere.

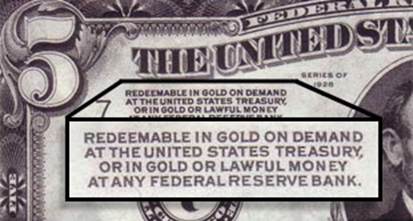

Figure 3 – A 1928 $5 bill. US dollar bills used to be redeemable in gold. Image source: https://www.mining.com/web/breaking-gold-standard-disastrous-consequences/

This made commerce faster and more efficient, but it quietly reintroduced a familiar vulnerability: once money became a claim recorded in a ledger controlled by institutions, trust shifted away from physics and back toward human management. And historically, that shift has often been where monetary discipline begins to weaken again.

By the late twentieth century, the world had largely moved to fully digital money – fast, convenient, and global – but no longer anchored to a scarce physical asset.

Which brings us to a new question that had never been solved before: could you create something digital that retained the scarcity of gold – without its physical limitations?

The digital problem: why digital scarcity seemed impossible

By the late twentieth century, money had largely become digital. Most of the money we use today is not physical at all. It exists as entries in databases: numbers recorded in banking systems that track who owns what. This solved many of gold’s practical problems. Digital money moves quickly. Payments can happen across continents in seconds, and commerce scales far beyond what physical settlement ever allowed.

But digital money introduces a fundamental challenge: digital information can be copied perfectly. If I send you a digital photo, I still have the photo. If I send you a document, both of us now possess identical copies. That is how computers are designed to work.

But money cannot work that way. If I could copy digital money the same way I copy a file, I could spend the same money twice, or a thousand times. Economists and computer scientists call this the double-spend problem, and for decades it appeared unsolvable without a trusted central authority.

The solution society adopted was institutions. Banks, payment networks, and central banks maintain ledgers that record balances and verify transactions. When you make a payment, what actually happens is that trusted intermediaries update their databases to reflect a transfer of ownership. In other words, banks assume responsibility for preventing double spending.

This is not a trivial task. It is an enormous technical and operational challenge. Modern banking systems must keep vast ledgers synchronised across millions of accounts, operating continuously with extremely high reliability. Systems must be secure against fraud and cyberattack, constantly backed up, redundantly stored, and carefully updated – often while running on layers of legacy hardware and software built decades ago.

Maintaining uptime is expensive and difficult. Even small failures can cascade through payment systems. And when transactions move between banks or across countries, the complexity increases dramatically. Different institutions, legal frameworks, currencies, and settlement systems all have to coordinate safely.

Yet as ordinary users, we never see this machinery. From our perspective, payments appear simple. We tap a card, send a message, or click a button, and money moves instantly. Behind that smooth experience sits one of the most complex pieces of infrastructure modern society has ever built.

For a long time, this seemed unavoidable. If digital money required someone to maintain the ledger, then money in the digital world would always depend on trusted intermediaries. Which is why, for decades, economists and computer scientists assumed truly decentralised digital money was impossible – until someone proposed a different approach.

Bitcoin

What is Bitcoin, at its core? At its simplest, Bitcoin is a public ledger that is not controlled by any single institution and that can be verified by anyone.

That may sound abstract, but remember what we discussed above. Modern money already relies on ledgers. Your bank maintains one. Payment networks maintain others. Ownership exists because trusted institutions update databases. Bitcoin asks a different question: what if the ledger did not belong to anyone, and yet everyone could trust it?

The breakthrough proposed in 2009 was to distribute the ledger across thousands of independent computers around the world. Instead of one authority maintaining the record, many participants maintain copies simultaneously. Anyone can join the network, download the ledger, and independently verify the entire transaction history.

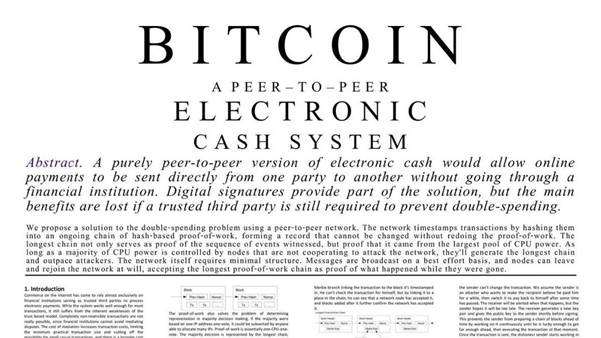

Figure 4 – The Bitcoin whitepaper by Satoshi Nakamoto, published 31 October 2008. Read the paper: https://bitcoin.org/bitcoin.pdf. Image source: https://bitcoinmagazine.com/culture/what-has-bitcoin-become-17-years-after-satoshi-nakamoto-published-the-whitepaper

But this immediately raises a problem. If nobody is in charge, who decides which transactions are valid? And how do participants agree on a single shared history without trusting one another?

Bitcoin’s answer combines three ideas: transparency, competition, and energy.

First, transactions are broadcast openly to the network. Every participant uses the ledger to checks whether the sender actually possesses the funds they are trying to spend. Because the ledger is public, verification does not depend on trust. It depends on mathematics and shared rules.

Second, transactions are grouped into blocks, and participants compete to add the next block to the ledger. These participants are known as miners. This is where energy enters the system. To add a block, miners must solve a computational puzzle that requires substantial real-world electricity and specialised hardware. The puzzle itself has no shortcut. The only way to solve it is through trial and error, performing vast numbers of calculations.

The first participant to find a valid solution earns the right to add the next block of transactions and receives newly created bitcoin as a reward. Because creating a block requires real energy expenditure, rewriting history would require redoing that same work and then surpassing the combined effort of the rest of the network. As the system grows, this becomes astronomically expensive.

Energy acts as a form of economic gravity anchoring the ledger to physical reality. Instead of trusting an institution, participants trust the fact that altering the record would cost more than anyone could reasonably gain. Over time, each new block builds on the previous one, forming a chain of blocks, what we call the blockchain. Changing a past transaction would require undoing all subsequent work, making the history increasingly secure as time passes.

The remarkable outcome is that strangers who do not know or trust one another can agree on a shared financial history without relying on a central authority. In effect, Bitcoin replaces institutional trust with verifiable rules and economic incentives.

And just as importantly, the rules governing supply are built into the system itself. New bitcoin are issued at a predictable rate, and that issuance decreases over time according to a schedule known in advance. No participant – not miners, not developers, not governments – can arbitrarily create more.

For the first time, scarcity exists in a digital system not because someone enforces it, but because the network collectively verifies it. Bitcoin, in this sense, is an attempt to recreate the monetary discipline of gold – but in a form native to the internet.

What problems Bitcoin attempts to solve

So if Bitcoin is a ledger designed to enforce scarcity and operate without central control, the next question is practical: what problems is it actually trying to solve in the real world?

The first is monetary debasement – something far more universal than many people realise. Across history, and across political systems, governments expand the money supply. Sometimes gradually, sometimes catastrophically. No country is entirely immune; the difference is mostly one of degree and speed.

In response, many people try to protect themselves by investing. They buy property, equities, or other assets in an attempt to outrun inflation. But that requires knowledge, access, stability, and risk tolerance. Markets fluctuate, investments fail, and large parts of the population, even in wealthy countries, hold savings in cash or low-yield accounts, leaving them exposed to the slow erosion of purchasing power.

Bitcoin’s first ambition is simple: to offer a form of money whose supply cannot be expanded in response to political or economic pressure. But its relevance becomes most visible not in stable environments, but in extreme ones.

Consider Venezuela.

After years of monetary collapse, inflation reached extraordinary levels, wiping out savings and salaries. Opposition leader María Corina Machado has described how hyperinflation destroyed the country’s financial system and how many Venezuelans turned to Bitcoin to bypass currency controls and preserve value. She called it a “lifeline” that helps citizens escape government-imposed exchange systems and safeguard their savings.

For refugees leaving the country, this mattered enormously. When national currencies collapse, physical cash often becomes worthless across borders. Bitcoin allowed some Venezuelans to carry savings digitally, something Alex Gladstein of the Human Rights Foundation has described as an emerging form of financial survival under authoritarian conditions.

A second use case appears in authoritarian environments where financial systems are used as tools of control.

Human rights groups and dissidents often struggle to receive funding because bank transfers can be blocked or monitored. According to the Human Rights Foundation, activists in countries such as Belarus used Bitcoin to send millions of dollars directly to striking workers after bank accounts were frozen during protests. Similarly, Bitcoin donations have supported pro-democracy movements in Nigeria’s EndSARS protests and opposition efforts in multiple restrictive regimes, precisely because transactions could occur outside traditional financial gatekeepers.

A third example involves remittances.

Cross-border payments remain surprisingly slow and expensive, particularly for people sending small amounts of money internationally. Traditional remittance systems can take days and charge significant fees. Bitcoin-based transfers allow individuals to send value globally without relying on correspondent banking networks – one reason populations facing currency instability or financial isolation increasingly experiment with it.

And finally, portability during crisis.

In wartime or political collapse, access to banks can disappear overnight. Accounts may be frozen, ATMs shut down, or withdrawals restricted. In such situations, wealth stored digitally but under personal control can become uniquely portable, something human-rights researchers increasingly describe as an “escape hatch” from financial repression.

Taken together, these examples illustrate that Bitcoin is not primarily solving problems for people whose financial systems already work smoothly. Its most immediate adoption often occurs where money itself has stopped functioning reliably – under hyperinflation, capital controls, censorship, or institutional breakdown.

That does not mean Bitcoin is perfect, or that it replaces existing systems. But it represents an attempt to create money that remains usable even when trust in institutions breaks down. In that sense, Bitcoin tries to combine three properties rarely found together in history: scarcity like gold, verification like software, and portability like information.

Trade-offs, criticisms, and open questions

At this point, it is important to step back and acknowledge that for all its strengths, Bitcoin is not a perfect system, and many of the questions surrounding it remain unresolved. Like any new technology – especially one attempting to redesign something as fundamental as money – it involves trade-offs.

The first and most visible is price volatility.

Because Bitcoin is still relatively young and adoption is uneven, its price can fluctuate dramatically. That volatility makes it difficult today to use as a stable unit of account or everyday spending currency in many contexts. For critics, this raises a reasonable question: can something so volatile function reliably as money?

A second challenge is usability.

Self-custody – the ability to control your own funds without intermediaries – is one of Bitcoin’s defining features. But it also introduces responsibility. Losing access credentials can mean losing funds permanently. While tools are improving, the user experience is still less forgiving than traditional banking systems designed around account recovery and customer support.

Third is the debate around energy consumption.

Bitcoin intentionally consumes energy as part of its security model. Supporters argue that this energy expenditure replaces institutional trust and secures a global monetary network. Critics argue that the energy cost is excessive or environmentally harmful. The debate continues, and reasonable people disagree, particularly about how Bitcoin mining interacts with energy markets and renewable power.

My personal view is that energy consumption is a feature and not a bug of Bitcoin – it is an indispensable way to anchor money in physical reality in a manner that cannot be faked. And it is emerging as a uniquely valuable technology for using stranded energy productively.

A fourth question concerns scale.

The Bitcoin network prioritises security and decentralisation, which limits how many transactions it can process directly. Additional layers and technologies are being developed to enable faster and cheaper payments, but whether these solutions will scale globally remains an active area of experimentation.

And finally, there are regulatory and political uncertainties.

Governments are still deciding how to treat Bitcoin – whether as an asset, a currency, a commodity, or something entirely new. Different jurisdictions are taking very different approaches, and future regulation will shape how widely and easily it can be used.

Taken together, these uncertainties mean Bitcoin should be understood not as a finished system, but as an ongoing experiment – one that has already operated for more than fifteen years without central control, but whose long-term role in the global monetary system remains unknown.

That uncertainty is important. The real question is not whether Bitcoin is flawless. The question is whether the problems it attempts to address are significant enough that societies continue exploring alternatives to existing monetary systems.

How to experience Bitcoin

At this point, a natural question people often ask is: How do you actually understand Bitcoin beyond theory? The honest answer is that, like many technologies, Bitcoin only fully makes sense once you use it, even in a very small way.

Importantly, this is not about investing or speculation. The goal is simply to observe how the system behaves. In South Africa, one straightforward way to try this is to download a regulated exchange or wallet application on your phone – for example, platforms such as VALR, Luno or others operating locally – and purchase a very small amount of bitcoin. The amount truly does not matter; even the equivalent of one or two hundred rand is enough for learning.

The interesting part comes next. You can send a small payment to another person in the room, or to a friend on the other side of the world, and watch what happens. Within minutes, value moves across the network without banks, without business hours, and without geographic boundaries.

Hundreds of thousands of outlets locally already accept Bitcoin payments, which allows you to see how digital settlement works in practice. Pick n Pay is one of them. I encourage you to go and buy a snack and a cold drink and pay for it in bitcoin, using a form of money that no government had a hand in creating.

Many people find that the moment they send or receive their first transaction, something clicks. Concepts that sounded abstract, like decentralisation, verification, and settlement, suddenly become concrete.

The important point is to approach this as an experiment. Start small. Assume you are paying tuition for learning rather than making an investment decision. Explore how wallets work, how transactions confirm, and how ownership is controlled.

Because regardless of where you ultimately stand on Bitcoin’s future, interacting with it directly provides insight into how digital systems can coordinate trust without central intermediaries.

[Image: AI-created]

If you like what you have just read, support the Daily Friend