The following is my address to the Biznews Conference, BNC#8, in Hermanus yesterday.

We’ve heard some fantastic talks over the last three days. I want to try to bring together some key threads as we assess what we’ve heard.

Over dinner yesterday I learnt a new word: “wipwaentjie”, which is the Afrikaans word for a rollercoaster. And that is a good word for the mood at this conference – a definite tension between hope and gloom.

There is a second tension that I’ve detected at this conference, and that is the tension over what to do – and what you can do. So let me address those two tensions in turn.

We’ll begin with the state of the country. Has SA turned the corner?

A few weeks ago, the finance minister told South Africans that we had reached “an important turning point” in the management of our public finances.

The Budget Review used similar language. It said the economy’s recovery was “starting to gain traction”. That, in a sentence, is the mood of the moment. South Africa, we are told, is turning the corner.

Now, at a conference like this, among investors, businesspeople, and people who have sat through three days of analysis, that claim is going to get one of two responses. Some people will say: at last. Others will say: not so fast. I want to suggest that both responses are partly right.

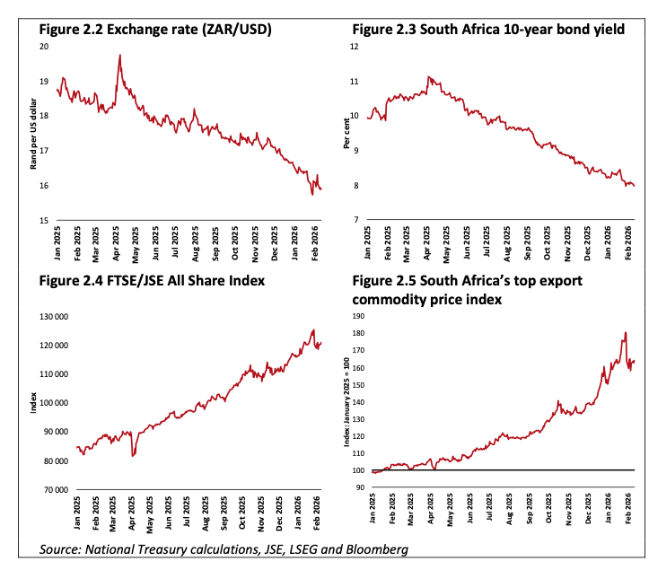

At the superficial level, the case for optimism is easy to make. Bond yields have come down from around 11% at the time of the 2024 election to around 8.5% now, having even dipped below 8% in February, before hostilities kicked off in the Middle East.

Business confidence has improved from 109 points when the Government of National Unity was formed in June 2024 to 131 points in January 2026, the latest numbers available.

We’ve just received the latest GDP growth figures, 1.1% for 2025. That means a doubling of the 0.5% recorded in 2024. National Treasury now expects growth of 1.6% in 2026, with a 1.8% average over the next three years. That sounds like growth is accelerating.

The inflation target has been lowered to 3%, with a +/- 1 percentage point tolerance band. Load-shedding dropped sharply from March 2024 and was suspended in May 2025. The GNU has proved more durable than many expected. And there is at least some continued movement, however halting, toward greater private participation in electricity, ports, and rail.

If you wanted to make the bullish cocktail-party case, you could do it in one breath: the fiscus is stabilising, reform is inching forward, inflation is lower, business confidence is up, and South Africa is finally behaving like a normal emerging market again.

Figure 1 – SA bullishness. Source: National Treasury, Full Budget Review 2026, p. 16,

But that is precisely where the caution must begin. Because none of that, on its own, means South Africa has turned the corner in the sense that really matters.

An economy growing at 1.1% is not turning the corner. It is limping less badly. An economy growing at 2% is not turning the corner either. Frankly, even 3% would not be enough to repair the social and economic damage South Africa has accumulated over many years.

The deeper problem is that our fixed investment rate remains far too low. The IRR’s latest growth strategy paper makes the point bluntly: South Africa has been stuck in a low-growth rut for over a decade. In inflation-adjusted terms, fixed investment fell from R775 billion in 2008 to R660 billion in 2024. As a share of GDP, it fell from 21.6% to 14.5% over the same period.

Without a decisive rise in capital formation we are not going to get the growth, jobs, or income gains we need. The same paper argues that if South Africa is to generate around 900,000 net new jobs a year, we will ultimately need real GDP growth of roughly 6% to 8%. That is what serious escape velocity looks like. Everything else is drift with a better press release.

And we should beware another South African habit: mistaking a tailwind for a turnaround. Commodity prices move in our favour, the rand firms, gold runs hot, platinum has a moment, and suddenly we begin talking about national renewal.

But a country that depends on a good external cycle to feel good has not turned the corner. It has simply enjoyed the weather.

Treasury itself says that faster reform in electricity, transport, and water is what would unlock materially higher investment and growth. In other words: even the optimists in government know that the current uplift is not enough.

So that is the superficial level. There is some real improvement and it should not be dismissed. But it should also not be confused with a durable shift in South Africa’s trajectory.

Now let me move to the deeper level, because this is where things become more interesting.

To understand whether a country is really turning the corner, you have to look beneath the market mood and ask a more fundamental question: are the politics beginning to align with the values and priorities of voters?

Because if they are, policy can change. And if policy can change, investment can rise. And if investment can rise, then growth can become self-sustaining rather than cyclical and borrowed.

This is where some genuinely significant things are happening.

Let me start with something that caught my eye last week. News24, for many years one of the country’s most important agenda-setting platforms, ran a strikingly critical piece on BEE under the headline: “BEE and EE: Criminalise cronyism, focus on the poor”.

It argued that while BEE helped deracialise ownership and create a black upper and middle class, it had fallen short of meaningfully reducing poverty for the majority, and that corruption, rent-seeking, and fronting had distorted its effects.

That is a serious crack in a long-standing elite consensus.

Why does it matter? Because for years South Africa’s mainstream debate allowed criticism of outcomes, but not criticism of core policy architecture.

You could say crime was bad. You could say corruption was bad. You could say government service delivery was bad. But once you started asking whether race-based laws, procurement premiums, or empowerment structures were themselves part of the problem, the room used to go cold.

That room is no longer as cold as it was.

And this tells us something important about the role of institutions like the IRR. A serious think tank is not supposed to be a comfort blanket. It is supposed to be a mirror, an early warning system and sometimes a pebble in your shoe. It is supposed to be out of step with its moment when its moment is wrong.

The IRR has done that for a very long time. It has been publishing the South Africa Survey every single year since 1947. It has existed since 1929. It opposed race laws under apartheid, and it opposes race-based laws now. Often that has meant being early and often that has meant being unfashionable. Even unpopular. But in democratic societies, that is often exactly the job.

Now look at the polling.

The 2024 election was a structural break. ANC dominance was broken. For the first time in democratic South Africa, the governing party was forced into power-sharing at national level.

Of course, that did not guarantee reform and as a matter of fact serious reform has been sorely lacking. But the loss of ANC dominance has changed the political mathematics. Opinion polling since the 2024 election suggests that the old political equilibrium, where the ANC called all the shots, is not coming back.

IRR polling conducted in March and April 2025 found the DA on 30.3% among registered voters and the ANC on 29.7%. It also found black support for the DA rising from around 5% historically to 18% in this polling round. Even the report’s authors are careful about the provisional nature of these findings. But even though they are provisional, it does seem that something has shifted.

The second important finding is even more powerful. When South Africans are asked what actually matters to them, they do not answer the way much of our political class talks.

In IRR polling, jobs and unemployment remain overwhelmingly the top priority. No other issue comes close. The report says job creation is the top issue across 27 of 28 respondent breakdowns.

It also notes the relative unimportance, as voter priorities, of issues like inequality, racism, health care, and land reform compared with jobs. That is a massive gap between elite fixation and popular concern.

When voters are asked what sort of policy they prefer, the answers become even more awkward for the current order.

Asked whether government should concentrate on raising employment or expanding welfare, 77.8% choose job creation, while only 19.9% prefer enlarged grants.

Asked how the state should spend procurement money, 81.7% say it should pick the best-priced supplier.

Asked whether vouchers for schooling, health care, and housing would help people get ahead more than current AA and BEE policies, 76.3% choose vouchers, with support for the individual voucher ideas in the mid-80s. Among black respondents, nearly four out of five say vouchers would be more empowering than AA/BEE. Among ANC supporters, 77.3% prefer vouchers to AA/BEE. That is not a fringe view. That is a democratic signal flare.

In other words, the deeper story in South Africa is not yet that the economy has turned the corner. It is that the politics may slowly be starting to.

That is the real basis for conditional optimism.

Because once politics begins to reflect voter priorities more honestly, policy change becomes possible. And once policy change becomes possible, South Africa’s upside is enormous.

What policies matter most? I would put three at the top.

First, race-based laws. South Africa cannot become a high-investment, high-growth economy while clinging to a legal architecture that classifies, penalises, distorts, and raises the cost of doing business.

The IRR’s No More Race Laws Bill is deliberately blunt in its title because the problem is blunt in reality. It proposes repealing race-based statutory preferences, replacing them with a non-racial, merit-based approach that we call Economic Empowerment for the Disadvantaged or EED, and ending the state’s reliance on official racial classification.

Whether one agrees with every clause or not, the direction is clear: stop governing a future economy through the bureaucratic categories of the past.

Second, property rights. Secure property rights are not a luxury good for the rich. They are the precondition for mass investment, urban development, small business formation, mortgage lending, and the broadening of ownership.

The IRR’s Right to Own Bill is not only about repealing expropriation without compensation. It is also about title deeds, housing vouchers, faster registration, use of underutilised state land, and stronger law enforcement against unlawful occupation and corruption. It is about turning property from a source of fear into a platform for growth.

Third, value for money and state capability. South Africa bleeds growth not only through ideology but through waste.

The IRR’s Value for Money Bill would make value for money the decisive standard in procurement, prohibit points-based award systems that undermine it, require transparent publication of reasons for awards, and put speed and payment discipline back into the system.

Again, whether one supports every detail or not, the principle is exactly right: poor South Africans do not benefit when the state overpays politically connected suppliers. They pay for it.

These proposals sit within a broader framework. The IRR’s growth strategy paper argues for four linked moves: increase direct investment, rebuild infrastructure, draw millions more into the labour market, and broaden economic participation in ways that actually work. It is a programme grounded in the simple proposition that South Africa must become a country that produces more, builds more, hires more, and trusts its citizens more.

If we do those things, then yes, South Africa becomes a serious candidate for strong capital inflows. Not because investors are sentimental or because they owe us anything, but because the country has real assets: location, mineral endowment, deep capital markets, substantial private-sector capability, good parts of an institutional inheritance, entrepreneurial talent, and a population that is still, for all the damage done, hungry for progress.

The missing ingredient is not potential. It is permission: permission, through policy, for South Africa to work.

That brings me to the final risk, and perhaps the most insidious one: despondency.

Ipsos found in September 2025 that 80% of South Africans thought the country was heading in the wrong direction. A Brenthurst Foundation survey found 70% saying the same. That kind of pessimism affects consumption, investment, risk appetite, social trust, and national ambition. It tells people not to build, not to stay, not to try, not to believe.

And yet despondency can become a form of vanity. It allows us to sit back and say: I knew it, this place is hopeless. But countries are not rescued by people who are merely correct about decline. They are rescued by people who are prepared to fight for a different outcome. People like you, the people in this room.

What can you do? You can register to vote and encourage all of your friends to do so, then go and make your mark on election day. Don’t be complacent about this, else you place yourself at the mercy of people who are not complacent.

Second, speak up. This has been a recurring theme at this conference. I know it’s hard for businesses to do so. But they should not underestimate the impact of a statement like: “Yes, we comply with BEE because the law forces us to. But we do so under duress. BEE is harming our business and it is harming the economy. We are investing less and creating fewer jobs because of it. We find it abhorrent to classify our employees by race. We do not support this kind of fake transformation.”

Third, give your financial support to the organisations that place themselves in the line of fire to rescue South Africa. Support the political parties that have sane economic policies and are meritocratic. And support the civil society organisations that fight every day against harmful policies, like the IRR and many other great organisations that we have heard from at this conference.

So, coming back to my initial question: has South Africa turned the corner?

At the superficial level, not yet. Some indicators have improved. We should welcome that. But it is still too little, too fragile, and too dependent on conditions we do not control.

At the deeper level, perhaps yes. Not economically yet. Politically, potentially.

We may be beginning to see the slow emergence of a South Africa in which voter priorities start disciplining political behaviour. If that continues, policy can change. If policy changes, investment can rise. If investment rises, growth can accelerate. And if growth accelerates, then this country can surprise the world very quickly.

That is the conditional optimism I would leave you with tonight.

South Africa is not a lost cause. But it is not a self-saving cause either. It will require argument. It will require courage and institutions willing to tell the truth before it is fashionable. That is part of what the IRR tries to do through its polling, its Blueprint for Growth papers, its Freedom Bills, and its broader #WhatSACanBe campaign.

So my message to you is simple: do not confuse green shoots with a harvest. But also do not miss the significance of the political opening that may be emerging. If we use it well, if we win the policy argument, if we move from anti-growth dogma to pro-growth reform, then South Africa will not merely have turned the corner. It will begin to run.

And that is a country worth backing.

[Image: John Endres, addressing the Biznew conference yesterday. Supplied]

If you like what you have just read, support the Daily Friend