South Africa’s current and proposed mining policies have made it the fifth least attractive country for mining investment, according to the “Policy Perceptions Index” (“PPI”) included in the Fraser Institute’s 2025 Annual Survey of Mining Companies.

By contrast, Botswana scores second best in the world on this PPI. The IRR’s Growth and Employment in Mining (GEM) Bill, released today, mirrors key Botswana rules and aims to make South Africa’s mining industry “investable” again.

An “eviscerated” mining industry

The Mineral and Petroleum Resources Development Act (MPRDA) of 2002 has “eviscerated” South Africa’s mining industry, to cite the words of journalist Michael Avery. The Mineral Resources Development (MRD) Bill of 2025 – which is intended to repeal and replace the MPRDA – will generally make bad law even worse. The effect will be to make a key industry still more “uninvestable”.

Despite having one of the richest mineral endowments in the world, South Africa’s attractiveness to mining investors has steadily declined since the MPRDA came into force in 2004. By comparison, its Botswana neighbour – which has good mining policies but far less mineral wealth – has thoroughly outpaced it on the authoritative Annual Survey of Mining Companies compiled by the Fraser Institute, a civil society organisation in Canada.

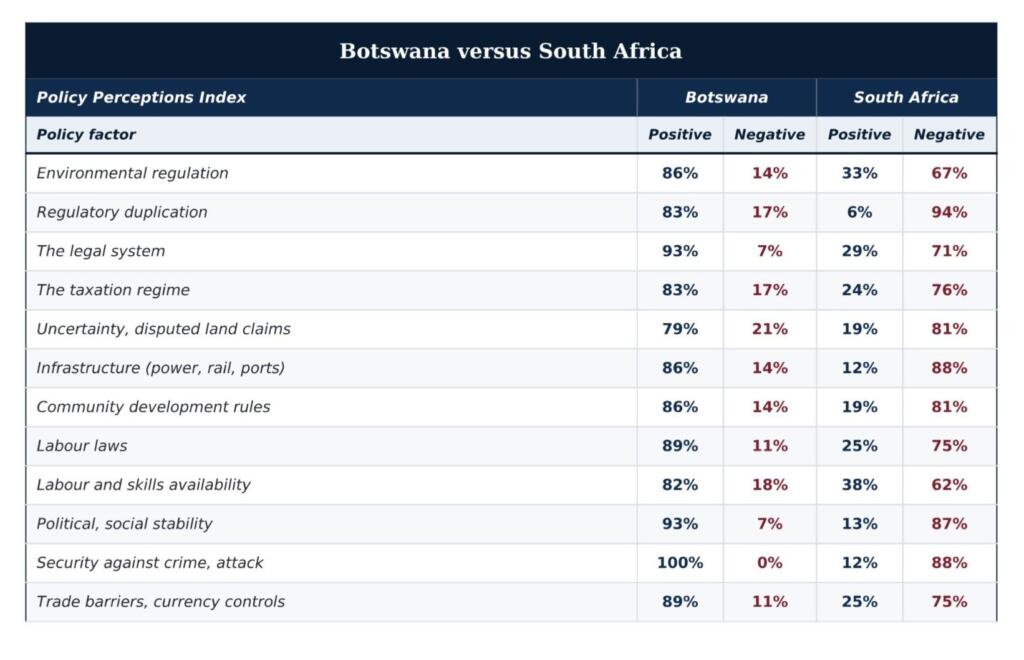

Botswana versus South Africa on the Fraser mining index

The 2025 Fraser Institute report, the most recent available, shows how wide the gap between the two countries has grown. Botswana’s clear and objective policies put it in 7th place out of 68 mining jurisdictions on the overall “Investment Attractiveness Index” (“IAI”), which takes account of both policy issues and mineral potential. On the “Policy Perceptions Index” (“PPI”), which assesses how policies affect investment attractiveness, Botswana has risen to 2nd best in the world.

By contrast, South Africa dropped to 57th out of 68 on the overall IAI, placing it almost in the bottom ten. It scored even worse – in 64th place out of 68 – on the PPI. Here, South Africa has scored the equivalent of an “own goal.” Governments cannot change their country’s mineral endowments, but they do control the mining policies that either attract or repel investors.

The PPI is based on 15 “policy factors” relevant to investment attractiveness. It assesses whether polices in each of these spheres either encourage investors to commit their capital or are such damaging “deal-breakers” as to drive them away. Comparing Botswana and South Africa on 13 of these 15 policy factors is illuminating.

Let’s start with the first on the Fraser list: “Uncertainty concerning the administration, interpretation and enforcement of existing regulations.” Here, 90% of investors see Botswana’s rules either as encouraging investment or as neutral in the sense that they do not “deter” it. By contrast, a mere 10% of investors regard these rules as an active deterrent to investment or a “deal-breaker.” On this policy factor, thus, investors view Botswana as 90% positive or neutral – let’s call it “positive” for short – and 10% negative.

In South Africa, by contrast, the situation is the opposite. Only 10% of investors see its existing regulations and their implementation either as encouraging investment or as neutral in not deterring it. By contrast, 90% see its existing rules as an active deterrent or a deal-breaker. The verdict on South Africa is thus 10% positive, versus 90% negative.

Botswana versus South Africa on 12 other “policy factors”

How do the two countries rank on 12 other policy factors, on this positive versus negative assessment?

Deeply damaging PPI scores for South Africa

South Africa’s PPI scores are deeply damaging, whereas Botswana’s are a drawcard. The discrepancy helps explain why GDP per capita in small and land-locked Botswana stood at some $19,100 in 2025 (in constant, inflation-adjusted or PPP dollars) – and significantly exceeded South Africa’s equivalent figure of $14,200.

If South Africa was ranked first or second in the world on the PPI, it could use this – together with its extraordinary mineral wealth – to trigger an upsurge in mining investment, growth and employment. Policy attractiveness of this kind would soon see its GDP per capita overtake Botswana’s and rise to levels more in keeping with its intrinsic economic strengths.

The IRR’s GEM Bill is intended to help bring this about. It mirrors Botswana’s Mines and Minerals Act of 1999 in some respects, particularly in introducing clear and objective rules for the granting of mining rights. It also seeks to replace a host of other damaging rules in the MPRDA and the proposed MRD Bill.

The GEM Bill needs to be accompanied by many other reforms, as set out by the IRR each year in its eight Blueprint for Growth policy papers. However, even without these further policy shifts, the GEM Bill would help to make the mining industry “investable” again.

Certain and non-racial rules

Like Botswana’s law, the GEM Bill makes the granting of mining rights solely dependent on clear and objective criteria: whether applicants have the technical and financial capacity to carry out approved mining operations, comply with health and safety rules, and remediate environmental damage. This dispenses with the current need for applicants to develop suitable “social and labour” plans: an MPRDA obligation that bureaucrats can interpret in many different ways. This encourages corruption. The GEM Bill also does away with damaging and ever-shifting black economic empowerment (BEE) requirements in the granting of mining rights.

Instead, the GEM Bill replaces BEE with a non-racial system of “Economic Empowerment for the Disadvantaged” (“EED”). EED has three core features. First, EED identifies disadvantage by income rather than race, thereby advancing the poor rather than enriching a small black elite. Second, it introduces a new EED scorecard that allows mining companies to earn voluntary EED points for their vital contributions to investment, growth, employment, export earnings, tax revenues, mine health and safety, and environmental stewardship.

Third, EED redirects much of the tax revenues being badly spent by bureaucrats on dysfunctional public schooling, housing and healthcare into tax-funded vouchers for the poor. EED’s schooling, housing and healthcare vouchers aim to give low-income households a real choice between public and private suppliers. The vouchers will end virtual state monopolies and incentivise all suppliers, including public ones, to compete for the custom of voucher-bearing families. Little could be more liberating for the disadvantaged – or more effective in keeping costs down and pushing quality up.

Alternatives to other damaging rules

The GEM Bill addresses many other problems in the MPRDA and the MRD Bill. The GEM Bill gives mining companies a necessary security of mining titles by reducing the scope for the arbitrary cancellation of their mining rights. It also protects mining land, mining rights and other property by requiring the payment of “prompt, adequate and effective compensation” on all expropriations.

The IRR’s alternative bill rejects compulsory beneficiation too. Instead, it leaves it to mining companies to smelt or otherwise process minerals inside South Africa where this makes economic sense. There is nothing to be gained from demanding local smelting when costly electricity supply and poor logistics make South African producers uncompetitive with China.

On mine closure, the GEM Bill allows companies that have remediated to required standards to obtain “clean” closure certificates. By contrast, the MRD Bill seeks to impose on them permanent environmental liability for latent impacts that might come to light only decades after closure – when the causal link to earlier mining is unclear.

The GEM Bill has a better solution, for it establishes a national pooled remediation fund, to which all mining companies must contribute in proportion to their overall remediation costs. These pooled monies will then be available to finance the remediation of latent post-closure impacts when these come to light. They could also help remediate historical damage from abandoned mines.

In addition, the GEM Bill dispenses with internal appeals to the mining minister, which delay the resolution of disputes and conflict with the separation-of-powers doctrine. Instead, it establishes an expert and Independent Mining Tribunal, with an appeals tribunal too. It also allows mining companies to refer all disputes to independent international arbitration, if they so choose.

#WhatSouthAfricaCanBe

The African National Congress (ANC) has long had the reverse of the Midas touch, for the policies it has implemented in pursuit of a socialist utopia have not turned dross to gold. Rather, they have built up barriers that keep investment out, growth down, and some 12 million South Africans jobless and destitute.

Fortunately, however, the great majority of voters no longer believe in the ANC’s false promises and want true transformation. In the mining sector, the GEM Bill gives practical content to the key reforms required.

Like the various other alternative bills the IRR has crafted over the past year, the GEM Bill helps to show #WhatSouthAfricaCanBe once it escapes the heavy hand of a corrupt and dysfunctional state committed to a coercive and destructive ideology.

[Image: By Shahir Chundra – Own work, CC BY-SA 4.0, https://commons.wikimedia.org/w/index.php?curid=63483934]

If you like what you have just read, support the Daily Friend